- April’s UK inflation data was worse than feared. Food and energy costs eased, cutting the headline rate from 10.1% to 8.7%. But core inflation reached 6.8%, the highest since 1992.

- The Bank of England thus faces the risk of inflation expectations becoming unanchored from its 2% target unless it takes further action.

- We expect the BoE to make two more 25bps rate rises in June and August now, lifting its Bank Rate to 5.00% to curb persistently inflationary pressures and rising wage growth.

- The GBP, however, is unlikely to benefit from further hikes. Elevated inflation may keep UK real interest rates negative in 2023 while the BoE needs to force a recession to curb inflation.

April’s UK inflation data was worse than feared. Easing food and energy costs reduced headline inflation from 10.1% to 8.7%. But core inflation rose to 6.8%, its highest since March 1992, as the prices of goods and services, excluding food, energy, alcohol and tobacco jumped 1.3% last month.

Source: Bank of Singapore, Bloomberg

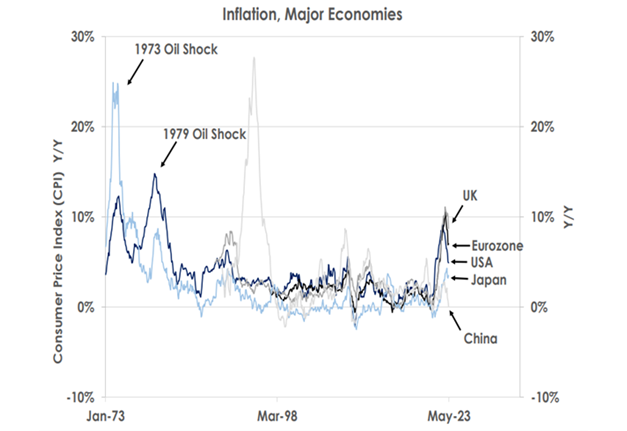

The chart shows UK inflation remains well above levels in the Eurozone, US, Japan and China and far higher than the Bank of England’s 2% target.

The BoE thus faces the risk of inflation expectations becoming unanchored from its 2% goal unless it takes further action.

We expect the BoE to make two more 25bps rate hikes in June and August now, lifting its Bank Rate to 5.00% to curb persistently inflationary pressures.

Source: Bank of Singapore, Bloomberg

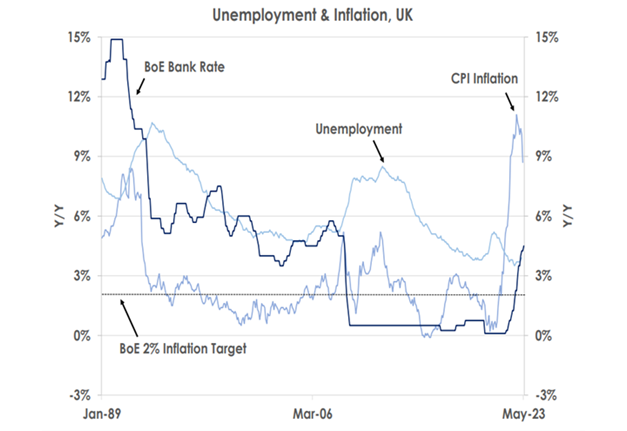

UK inflation is being driven by the rising costs of core goods and services and by stronger wage growth. The chart above shows unemployment is just 3.9% despite the BoE increasing interest rates from 0.10% in 2021 to 4.50% now. The tight labour market has caused weekly earnings to rise 6.7% over the past year, further fuelling inflation.

Source: Bank of Singapore, Bloomberg

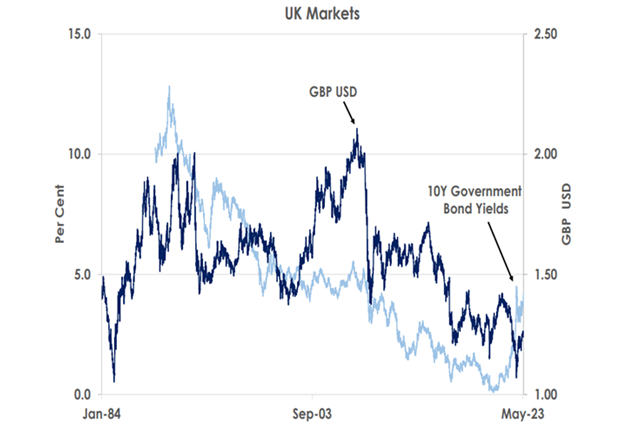

The BoE thus needs to raise interest rates more to break any ‘wage-price spiral’. But the GBP is unlikely to benefit.

First, elevated inflation is set to keep real interest rates negative. Core inflation may exceed the Bank Rate for the rest of 2023.

Second, we think the BoE will need to engineer a recession to curb inflation. We forecast the GBP to stay below 1.25 against the USD over the next 6 months and GDP to shrink 0.3% in 2023, keeping us cautious on the UK economic outlook.

This article was first published by Bank of Singapore on May 25, 2023. The Opinions expressed in this publication are those of the authors. They do not purport to reflect the opinions or views of Bank OCBC NISP Private Banking Tbk. or its affiliates.

OCBC NISP Private Banking provides a suite of products for wealth creation, preservation and transmission including holistic wealth management services, independent research, customized solutions for all investor preferences, and genuine open architecture, with expertise in Indonesia and Asia Pacific markets. OCBC NISP Private Banking is a part of OCBC Group.