Overnight, the Federal Open Market Committee left its fed funds rate at 5.25-5.50% as widely expected.

The FOMC noted 'in recent months, there has been a lack of further progress toward the Committee's 2 percent inflation objective’ while Federal Reserve Chairman Powell said ‘so far this year, the data have not given us that greater confidence [that inflation is falling towards the Fed’s 2% target] … it is likely that gaining such greater confidence will take longer than previously expected.’ Thus, the FOMC meeting was also in line with investor expectations that higher inflation prints for January, February and March would cause the Fed to delay the start of rate cuts and reduce the likely number of moves to only a couple of 25bps cuts now this year.

Ahead of the meeting, 10Y Treasury yields had surged to as high as 4.73% - not far from last year’s peak of 5.00% and up sharply from 3.75% at the start of the year - as investors had begun to fear the Fed would have to resume rate hikes to curb inflation. But aside from signalling interest rate cuts would be delayed, the rest of the FOMC meeting was dovish, causing 10Y yields to fall back to 4.60% overnight.

Firstly, Powell made it clear the bar to resume rate hikes was high: ‘I think it's unlikely that the next policy rate move will be a hike. I would say it's unlikely’.

Secondly, Powell observed the Fed’s interest rates were already likely to be restrictive enough to keep slowing the economy and lowering inflation.

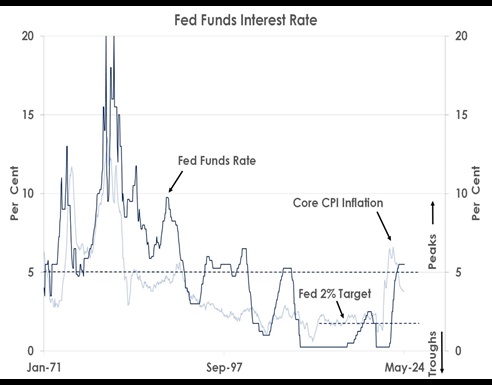

Source: Bank of Singapore, Bloomberg

‘I do think that the evidence shows pretty clearly that policy is restrictive and is weighing on demand. And there are a few places I would point to for that. You could start with the labor market. So, demand is still strong … but it's cooled from its extremely high level of a couple of years ago … you see in spending, like house and investment, you also see that higher interest rates are weighing on those activities. I do think it's clear that policy is restrictive.’

Thirdly, Powell signalled interest rates would stay at their current 23-year highs for longer to reduce inflation rather than being raised again.

‘We're committed to retaining our current restrictive stance of policy as long as it is appropriate.’

Lastly, the Fed said it would start in June to taper the pace at which its balance sheet is contracting. Thus, it will slow its quantitative tightening (QT) despite core inflation remaining near 3-4% at present.

In short, the dovish Fed seems keen not to shock investors by pivoting back towards rate hikes. Though officials will want to see core consumer price rises - excluding food and energy - moderate from 0.3-0.4% a month so far this year to 0.1-0.2% increases, we think the Fed still seems likely to make two 25bps rate cuts this year. We thus forecast 10Y Treasury yields to return to 3.75% over the next 12 months - to the benefit of bond markets broadly - rather than exceed last year’s peak of 5.00% again.

This article was first published by Bank of Singapore on May 2, 2024. The Opinions expressed in this publication are those of the authors. They do not purport to reflect the opinions or views of OCBC Private Bank or its affiliates.

OCBC Private Bank provides a suite of products for wealth creation, preservation and transmission including holistic wealth management services, independent research, customized solutions for all investor preferences, and genuine open architecture, with expertise in Indonesia and Asia Pacific markets. OCBC Private Bank is a part of OCBC Group.