The CHIP-EP framework for AI: Investing through the verses and choruses of the AI supertrack

- We believe the artificial intelligence (AI) supertrend unfolds in distinct phases and a structured framework could help investors identify the next wave of value creation while avoid overpaying for yesterday’s winners.

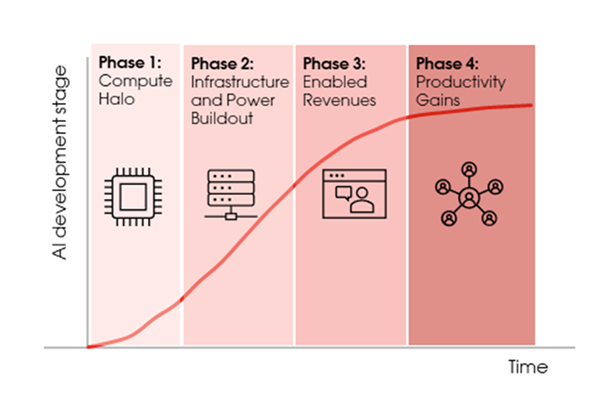

- We introduce the CHIP-EP framework, whose name is symbolic of how the AI supercycle powered by chips will be on an EP, or “extended play” as referred to in musical releases - (Phase 1) Compute Halo, (2) Infrastructure and Power buildout, (3) Enabled revenue and finally (4) Productivity gain.

- We are at the cusp of transitioning from Phase 2 of Infrastructure and Power buildout, where compute scaling is prioritised over profitability, to Phase 3 of Enabled Revenue which is characterised by monetisation of AI products and emergence of purpose-built Small Language Models (SLMs).

- Portfolio implication 1: New high growth subsegments will emerge in the physical infrastructure layer in the coming years as compute demand shifts from AI training towards AI inference that better supports AI applications with low latency and cost effectiveness i.e. CPU, inference-specific ASICs, memory, storage and networking. Meanwhile, GPU plays could evolve into core, stable growth holdings.

- Portfolio implication 2: Selectivity and patient capital are required for investors entering software names now as near-term sentiment could remain subdued with AI disruption weighing on growth over the next 3-5 years. In the longer run, however, we expect AI to expand software’s addressable market and even surpass semis’, albeit alongside a reshaped competitive landscape with new entrants.

AI’s supertrend is durable, but alpha depends on phase‑aware portfolio construction

AI has rapidly transitioned from a niche technological domain into a foundational economic force since ChatGPT debuted in 2022, rivalling other major innovation cycles in the past that easily lasted decades. For investors, this evolution has not been linear; rather, it has unfolded in distinct phases, each with different winners, value drivers and risk profiles. As a result, a structured investment framework is essential for navigating the shifting landscape and identifying the next wave of value creation.

The early phase concentrated value in “picks-and-shovels” providers supplying the foundational infrastructure and was characterised by a surge in demand for compute power. Training large AI models requires enormous computational resources, driving demand for GPUs / AI accelerators. As infrastructure scaled, attention shifted to firms’ ability to monetise AI. Cloud providers embedded AI into their ecosystems while enterprises began experimenting with AI deployment.

In short, AI investing is not about a single winner - it is about identifying where value accrues at each stage. Without a structured framework, investors risk overpaying for yesterday’s winners (e.g. chasing semiconductors after peak margins), underestimating second-order beneficiaries and missing inflection points in adoption cycles. History demonstrates the challenges of maintaining rapid sales growth and extremely high margins. Between 1985 and 2024, there have been just 121 unique S&P 500 companies that historically been able to grow sales by 20%+ for five straight years (out of 1,065 unique non-financial companies in total). Over the same period, there have been just four unique S&P 500 companies that maintained EBIT margins over 50% for five consecutive years.

Hence, we are introducing a robust AI investment framework in the next section that evaluates two key parameters:

a. Phase of AI development, where we believe adoption follows a S-curve from initial excitement and experimentation to scaling and finally to normalisation.

b. Layer of the AI stack (foundation model, physical infrastructure, software & applications and end users of AI) where each layer has different capital intensity, margins, and competitive dynamics.

Identifying the current stage helps investors anticipate shifts in leadership. We would also differentiate value creation from value capture e.g. Large Language Models (LLMs) could be creating value for the entire AI ecosystem but their ability to capture value for themselves by charging users remains an unknown.

Introducing our 4-phase CHIP-EP framework

As with other revolutionary technological innovations in the past such as the internet, we believe the AI development and associated opportunities would follow a S-curve according to four phases – (1) Compute Halo, (2) Infrastructure and Power buildout, (3) Enabled revenue and finally (4) Productivity gain. The phases give rise to our CHIP-EP framework, which is symbolic of how we view the AI theme – AI, powered by chips, will be on an EP, or “extended play” as referred to in musical releases.

Exhibit 1: AI trade could play out in four phases along a S-curve

Source: Bank of Singapore

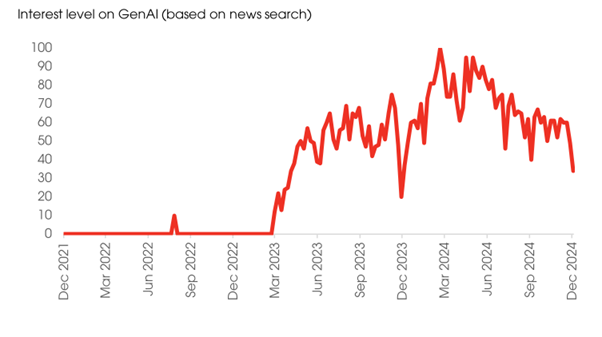

Phase 1: Compute Halo began to take shape in early 2023 following the launch of ChatGPT. This milestone sparked a surge of optimism, with market participants extrapolating the transformative potential of AI well ahead of tangible, scaled applications. As a result, public and investor attention intensified sharply, evident in elevated search activity and heightened media coverage. During this initial phase, focus was highly concentrated on a leading GPU player, widely seen as the most direct beneficiary given its clear technological leadership and first-mover advantage in AI compute infrastructure.

Exhibit 2: Halo effect around AI created as public interest surged after release of ChatGPT in 2022

Note: Numbers represent search interest relative to the highest point on the chart, with a value of 100 being the peak popularity for the term. Source: Bank of Singapore, Google Trends

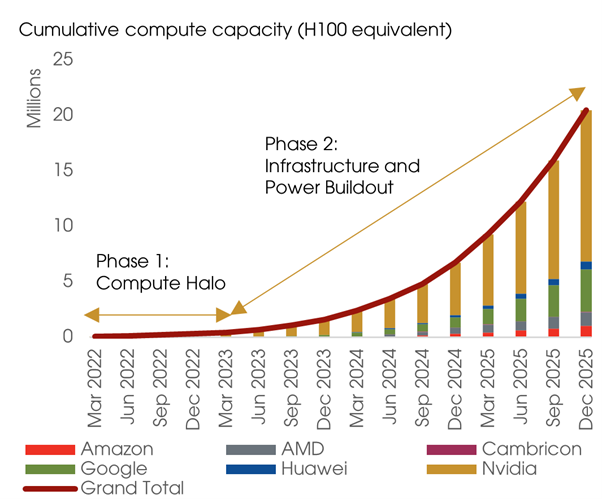

Phase 2: Infrastructure and Power buildout focus on scaling of AI compute, benefiting companies beyond GPU plays. Riding on the initial ebullience, companies and investors getting into the AI scene with an eye on future potential demand. Relatedly, a key characteristic of this phase is that immediate monetisation of AI investment is not a major concern.

In this phase, more players enter the fray at the infrastructure layer including at the LLMs (e.g. Gemini, Claude) and AI accelerators (e.g. custom chips) sub-layers. At the same time, more power is required to support the rapid buildout of physical infrastructure by cloud providers. A supply crunch of semi (e.g. GPU, HBM) ensues as production capacity increase lags the sudden inflection in demand. Heavy CAPEX by the cloud providers (which include hyperscalers) consequently generate high margins and profits for the semis players (from memory to GPU/ASICs), with some spillover also to utilities companies. Monetisation by the LLMs generally remain limited at this stage.

Exhibit 3: Exponential increase in compute capacity during Phase 2

Source: Bank of Singapore, Epoch AI

Phase 3: Enabled revenues will herald a period where companies incorporate AI in product offerings to boost revenues. This would likely begin with the tech sector which has the most intricate knowledge of AI, including the publicly listed hyperscalers as well as private AI natives. A leading private AI native, for one, has seen meteoric growth, crossing a USD30bn annualised revenue run rate in April 2026, up from USD9bn in end-2025 and USD1bn in end-2024. Even so, we could be at the start of a revolutionary wave that lasts well into the decade ahead. Taking a leaf from the mobile app history, it registered explosive growth in revenue and use cases for at least a decade that were unfathomable at the inception, while quietly transforming our daily lives.

As AI agents and other applications proliferate, we expect more diversification at the foundation model layer with Small Language Models (SLMs) taking up a larger share as they are more targeted with potentially lower latency and higher cost-effectiveness that can be deployed on edge computing.

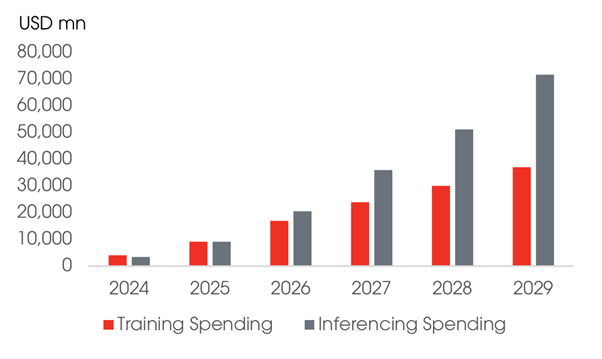

The main beneficiaries in the physical infrastructure will also start to shift from the AI training players towards the AI inference ecosystem due to the requirement for low latency, persistent compute and connectivity to a larger user base. The favoured subsegments will broaden from the GPU towards inference-specific ASICs, CPUs, DRAM/NAND in memory, storage and networking. Supply constrains could then shift from the AI training towards AI inference ecosystem in the early part of Phase 3. With substantially enough time (i.e. >three years), however, we expect AI physical infrastructure to eventually move towards a steady growth state where supply would have caught up and therefore resulting in a more stable supply-demand dynamics. Hyperscalers would also be monetising their earlier CAPEX, and we expect the cloud services provided to be differentiated between training and inference needs.

At such a point in the future, we believe value creation could continue via software and applications for many more years to come. It could play out in a similar fashion to the internet revolution whereby the internet companies continued to thrive long after the telecom and equipment vendors, the picks and shovels equivalent, lost their shine.

Exhibit 4: Inferencing spending is expected to accelerate and overtake training spending

Source: Bank of Singapore, Gartner

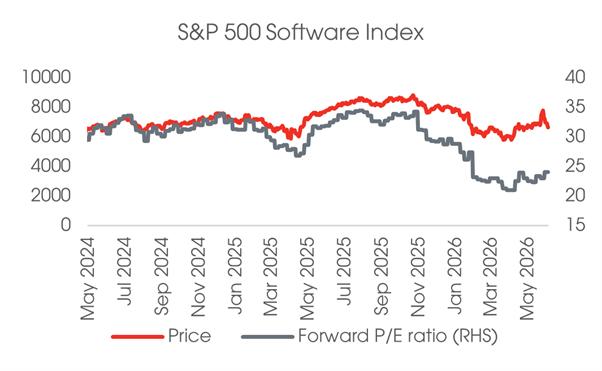

While software and IT services industries should be poised to incorporate AI to enhance their offerings, their incumbents are also among the most likely to be disrupted at the onset of Phase 3, particularly with faster-to-market offerings by AI natives and a transition from seat-based to consumption-based contracts. Hence, the current software sentiments have been sluggish as indicated by compressed valuations even as near-term earnings hold up. In addition, companies that began investing for AI early have yet to see significant enough monetisation to convince investors they are benefitting from it.

Ultimately, the key to a sustained shift in sentiment for software will be the disclosed AI revenue being additive to the whole company’s revenue growth. Software incumbents need to directly address their ability to innovate faster via: i) efficient adoption of AI tooling; and ii) a shift away from roles that are being automated toward roles that are directly tied to sales capacity or product innovation.

We are likely still in the early stages of AI application commercialisation and it could take a few more years to decisively tell which are the disruptors and which are the disrupted, although this period could also present alpha opportunities for patient investors with conviction on down beaten software stock’s moats.

Exhibit 5: Valuations of software companies have compressed on AI disruption fears

Source: Bank of Singapore, Refinitiv Workspace

Phase 4: Productivity gains will encompass a widening of sectors beyond tech, where AI is actively harnessed to improve productivity. The largest potential efficiency gains are most likely to be reaped from labour-intensive industries with jobs more exposed to AI automation. Sectors such as Software and Services and Commercial and Professional Services are among those which have the largest potential earnings boost from widespread AI adoption via labour productivity and thus stands to benefit the most.

Summary of Phases 1-4 in our CHIP-EP framework

Putting all the pieces together, the exhibit below captures which part of the value chain we favour in various AI phases.

Exhibit 6: Favoured investment segments (highlighted in green) during the various AI phases in our CHIP-EP framework

| Phases/ValueChain | 1: Compute Halo | 2: Infrastructure and Power Buildout | 3: Enabled Revenues | 4: Productivity Gains |

|---|---|---|---|---|

| Immediate, direct beneficiaries of early AI hype | Broader physical footprint required to scale computing power | Monetising AI capabilities through productisation | Non-tech companies using AI to aggressively lower operational expenses | |

| Foundation model | LLMs | LLMs | LLMs, SLMs | LLMs, SLMs |

| Physical infrastructure | AI accelerators | Primary beneficiaries are AI accelerators and memory (HBM), with spillover to utilities | Primary beneficiaries broaden to CPU, memory (DRAM/NAND), networking, storage etc | |

| Software and applications | Sub-segments/ single stocks with resilient moats and using AI as tailwinds | |||

| Users of gen AI | Beneficiaries beyond tech |

Note: LLM = Large Language Models, SLM = Small Language Models that are less compute intensive and have more targeted use cases. Source: Bank of Singapore

Assessing the current phase and near-term investment implications

We believe that we are transitioning from the late stage of Phase 2 of Infrastructure and Power buildout to the early days of Phase 3 of Enabled Revenue.

First, the days of indiscriminate buildout without a clear roadmap for monetisation, as characteristic of Phase 2 where there is still some euphoria, is likely behind us. A year or two ago, higher CAPEX announcements by the hyperscalers could result in higher share prices as the market prioritise gains in market share in the revolutionary tech over monetisation and profitability. However, we have observed that markets have begun to punish hyperscalers whose increased CAPEX result in negative free cash flow as of early 2026. For instance, Amazon’s share price plummeted by 16% over seven days from its 2 Feb 2026 closing price due to concerns that its announced CAPEX would result in negative free cash flow for 2026.

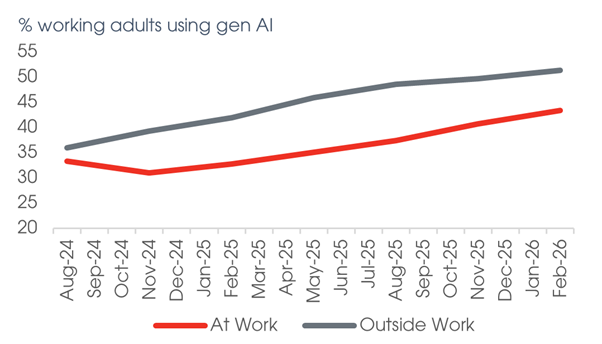

Second, AI adoption by end users is picking up but the level of utilisation remains nascent according to surveys. On balance, we are in the relatively early days of embracing the use of AI.

Exhibit 7: AI adoption is picking up both at work and outside of work

Source: Bank of Singapore, Gen AI Adoption Tracker

Third, there is more evidence that AI commercial applications are moving into the revenue generation stage. More importantly, Anthropic is reportedly on track to post its first profitable quarter in 2Q26, way ahead of its initial projections made in 2025 to only breakeven in 2028. That said, we are likely still in the very early innings and the success thus far is most evident in selected AI natives. Incumbent software companies’ AI offerings, if any, remain a small part of the overall revenue.

With successive rolling out of AI applications and more widespread usage among end users, the road ahead would imply the following for investors:

Physical infrastructure - As compute demand correspondingly shifts from AI training towards AI inference, we envision the growth semis subsegments in Phase 1 and 2, i.e. GPU, would become a core stable growth part of one’s tech portfolio in Phase 3, while new high growth subsegments emerge i.e. CPU, inference-specific ASICs, memory, storage and networking. For instance, Nvidia cited the Total Addressable Market (TAM) for CPU as USD200bn in late May 2026, which is substantially higher than the ~USD100bn figure quoted by competitors before that.

We think the trend of upward revision in TAM could have some more runway as AI agents open a new paradigm of having agents managing other agents and are not necessarily limited by the amount of human labour, in turn contributing to substantially higher AI inference needs. And this growth in demand could come faster than supply can catch in the coming few years, thereby creating a near- to medium-term supply constrain. That said, the growth subsegments of Phase 3 come with higher risk as well, particularly on the technological front where competition is intense e.g. LPU, CPU, NPU and TPU are but some of the contenders for inferencing compute.

Exhibit 8: The role of semi subsegments in a portfolio evolves from Phase 2 to Phase 3

| Phase 2 | Phase 3 | |

|---|---|---|

| GPU | Growth | Core/Stable |

| ASIC | Growth | Growth |

| Memory | Growth (mainly HBM) | Growth (broaden to DRAM/NAND) |

| CPU | - | Growth |

| Networking | - | Growth |

| Storage | - | Growth |

Source: Bank of Singapore

Software and applications – Near-term sentiments could remain subdued as AI-related deflation (e.g. margins compression) is expected to weigh on growth over the next 3-5 years before normalising, accompanied by some potential industry consolidation. At this juncture, we would advise selectivity and patient capital as it could take years for broad software sentiments to improve. However, in the longer run, AI is expected to be additive to the software’s TAM, which is expected to increase from about USD1tn in 2025 to USD1.7tn by 2030, while widening the gap with the USD1-1.1tn semi market in 2030 according to most assessments. Hence, it is a segment we would revisit in the future when moats and AI revenue generation of software companies become clearer as we venture deeper into Phase 3.

This article was first published by Bank of Singapore on 02 July 2026. The Opinions expressed in this publication are those of the authors. They do not purport to reflect the opinions or views of OCBC Private Bank or its affiliates.

OCBC Private Bank provides a suite of products for wealth creation, preservation and transmission including holistic wealth management services, independent research, customized solutions for all investor preferences, and genuine open architecture, with expertise in Indonesia and Asia Pacific markets. OCBC Private Bank is a part of OCBC Group.