China’s outlook is at a critical juncture. Its GDP jumped an impressive 2.2% QoQ in 1Q23 after the country reopened from the pandemic. But the economy only expanded by 0.8% QoQ in 2Q23 as confidence faded in the recovery. In 3Q23, growth has continued to be weak.

Source: Bank of Singapore, Bloomberg.

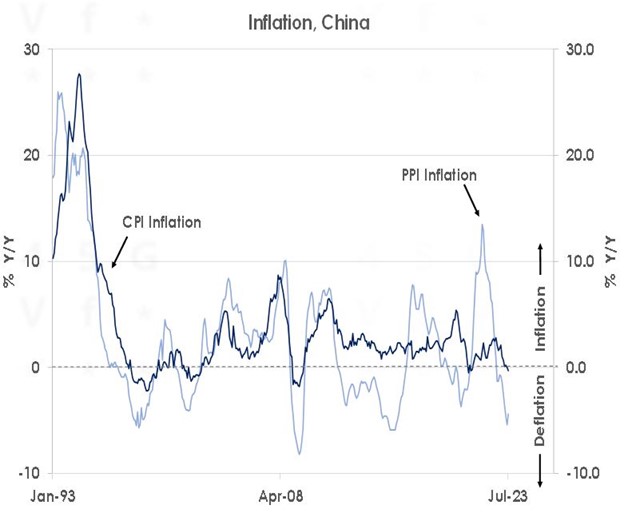

Despite this year’s reopening, China’s economy is suffering from a clear lack of demand.

For example, inflation has vanished as the chart above shows. In July, consumer price index (CPI) inflation fell into deflationary territory with prices 0.3% lower than a year ago. Excluding volatile food and energy costs, core inflation was still positive at 0.8% last month. However, China’s situation contrasts sharply with the US, Europe and Japan.

Source: Bank of Singapore, Bloomberg.

Similarly, purchasing manager indices (PMI) – a key measure of business sentiment – indicate confidence has declined sharply after an initial rebound in early 2023 as the next chart shows.

The shocks from 2020-2022 – strict lockdowns, regulatory hits, property weakness, recessions abroad and geopolitical risks – all appear to have hurt China’s engines of growth this year.

Source: Bank of Singapore, Bloomberg.

Firstly, consumers have turned cautious again.

The chart above shows retail sales were off the scale when China’s economy reopened in 2021 and again at the start of 2023. But the strict lockdowns of 2022 and 2022 have had a more longer lasting impact on consumer confidence.

In July, retail sales were only 2.5% higher than a year ago. In contrast, retail sales were expanding by 8.0% a year at the end of 2019.

Increased job insecurity during the pandemic, China’s limited social safety nets – despite its strict lockdowns, the government didn’t follow the US, Europe or Japan in providing large-scale support to households – and falling property prices are all keeping consumers cautious.

Source: Bank of Singapore, Bloomberg.

Secondly, investment is lacklustre.

In July, fixed asset investment was only 3.4% higher than a year ago, half its rate at the start of the pandemic in 2020.

In China’s manufacturing sector, investments priorities favoured by the government including electric vehicles and renewables are clear bright spots. But China’s regulatory shocks and America’s imposition of export controls have hurt sentiment in the tech sector.

In the property sector, falling real estate prices, unfinished projects and defaults by developers are causing households to delay new purchases. Thus, fixed asset investment in the sector is contracting by almost double digits as the chart above shows.

Infrastructure investment is also being held back. As the economy’s rebound from China’s reopening stalls, local government financing vehicles (LGFVs) are choosing to pay back debts – rather than borrow to undertake new projects. The following chart of total social financing (TSF) shows the broad measure of credit growth only expanded by 9.2% over the past 12 months to July.

Source: Bank of Singapore, Bloomberg.

Thirdly, exporters are suffering from weak demand abroad.

The UK and Eurozone have endured recession and stagnation since last year’s shock to energy prices from Russia’s invasion of Ukraine. Higher interest rates and inflation have also caused US consumers to slow down spending too this year.

Source: Bank of Singapore, Bloomberg.

In July, China’s exports were 14.5% lower than a year ago as the chart above shows. The CNY has weakened too with the currency close to 15-year lows around 7.30 against the USD despite efforts by the People’s Bank of China (PBoC) to support the exchange rate.

Faced with weaker-than-expected growth, policymakers have begun to respond with limited measures to revive demand.

New PBoC Governor Pan Gongsheng said the central bank would help property developers fulfil reasonable financing demands. The central government is allowing provincial governments to raise new funding to help local government financing vehicle refinance debts and the PBoC this month trimmed its key interest rates – by 10bps to 1.80% for its 7-day reverse repo rate and by 15bps to 2.50% for its 1Y medium-term lending facility as the chart below shows.

Source: Bank of Singapore, Bloomberg.

However, to stop China falling into a prolonged deflationary trap, officials will need to step up with concerted action on three fronts: major fiscal easing, efforts to stabilise the property sector and rapid interest rate cuts.

Source: Bank of Singapore, Bloomberg.

With three of China’s four engines of growth – consumption, investment and exports – under pressure, the most likely actor to revive demand in the economy is the government.

The last chart shows total debt owed by both local and central government in China is still relatively low as a share of GDP. Though local governments are unwilling to sharply increase investment on infrastructure as their financing vehicles pay down debt, China’s central government has the balance sheet to sharply boost consumption across the economy by transferring funds to households as governments in the US, Europe and Japan did during the pandemic.

Major fiscal easing would help accelerate growth again in China. The authorities could also support demand too by cutting interest rates more rapidly as the Federal Reserve and other major central banks managed during the crises of 2008 and 2020. With inflation so low in China, the PBoC has the scope to reduce interest rates aggressively to induce fresh demand for credit.

Lastly, officials need to take comprehensive action to stabilise China’s vast property sector. By supporting the completion of pre-sold homes, easing restrictions on new purchases and providing households with cash transfers, policymakers could help revive confidence in China’s real estate markets and temper the risk of falling prices making prospective buyers keep postponing their purchases.

Currently, we forecast China’s GDP to expand by 5.4% in 2023 – compared to lacklustre growth of just 3.0% in 2022 – as last year’s lockdowns fade. But for growth to reach our forecast, officials will need to undertake large-scale fiscal easing, cut interest rates more aggressively than the PBoC’s so far limited 10-15bps moves and take wide-ranging action to stabilise China’s property markets.

If policymakers remain reluctant to take decisive measures to revive demand and confidence in the economy, then China’s GDP growth is likely to fall short of the government’s 5% target in 2023. In that case, the risks of a more prolonged deflationary slump will increase.

This article was first published by Bank of Singapore on August 21, 2023. The Opinions expressed in this publication are those of the authors. They do not purport to reflect the opinions or views of Bank OCBC NISP Private Banking Tbk. or its affiliates.

OCBC NISP Private Banking provides a suite of products for wealth creation, preservation and transmission including holistic wealth management services, independent research, customized solutions for all investor preferences, and genuine open architecture, with expertise in Indonesia and Asia Pacific markets. OCBC NISP Private Banking is a part of OCBC Group.